However be mindful that short-term health insurance may have limitations that regular medical insurance does not have, such as caps on annual benefits paid. Medicare is a federal health insurance program for Americans above the age of 65. It provides free or greatly cost-reduced healthcare to eligible enrollees. There are 4 parts to Medicare that cover various healthcare services:Part A for inpatient (hospital) care, for which the majority of people pay no premiums Part B, for outpatient care, like medical professional's workplace sees. In 2021, Part B has a month-to-month premium of $148. 50.Part C, which is also called Medicare Advantage, and allows you to buy into private health insurance.Part D, for prescription drug protection. gov or your state exchange.

Medicaid is a federal and state medical insurance program for low-income families and individuals. Medicaid has eligibility requirements that are set on a state-by-state basis, however it is primarily developed for those with low earnings and low liquid assets. It is likewise developed to help families and caretakers of children in requirement. You can generally inspect if you receive Medicaid through health care. gov or your state exchange. The Kid's Health Insurance Program( CHIP) is a federal and state program that is comparable to Medicaid, but particularly designed to cover kids below the age of 18. Like Medicaid, you can normally see if you certify and use on Health care.

gov or your state's exchange. All personal health insurance strategies, whether they're on-exchange or off-exchange, work by partnering with networks of health care providers. But the way that these strategies deal with the networks can vary considerably, and you wish to make certain you comprehend the differences in between these plans.HMO plans are the most restrictive kind of strategy when it pertains to accessing your network of companies.If you have an HMO plan, you'll be asked to select a primary care physician( PCP) that is in-network. All of your care will be coordinated by your PCP, and you'll need a recommendation from your PCP to see an expert. HMO strategies usually have cheaper premiums than other kinds of personal medical insurance plans.PPO prepares are the least limiting kind ofplan when it comes to accessing your network of companies and getting care from outside the strategy'snetwork. Generally, you have the alternative in between choosing in between an in-network physician, who can you see at a lower expense, or an out-of-network physician at a higher cost. You do not require a recommendation to see an expert, though you may still select a primary care physician( some states, like California, may need that you have a main care doctor). PPO plans normally have more expensive premiums than other kinds of personal health insurance plans.EPO prepares are a mix in between HMO strategies and PPO strategies. Nevertheless, EPO plans do not cover out-of-network doctors. EPO strategies generally have more costly premiums than HMOs, however cheaper premiums than PPOs.POS strategies are another hybrid of HMO and PPO strategies.

You'll have a main care company on an HMO-style network that can coordinate your care. You'll also have access to a PPO-style network with out-of-network options( albeit at a greater cost). The HMO network will be more cost effective, and you will need to get a referral to see timeshare experts Take a look at the site here HMO professionals. POS strategies generally have more pricey premiums than pure HMOs, however cheaper premiums than PPOs. Discover more about the differences between HMOs, PPOs, EPOs, and POS plans. Some people get confused due to the fact that they believe metal tiers describe the quality of the strategy or the quality of the service they'll receive, which isn't true. Here's how health insurance coverage plans roughly divided the costs, arranged by metal tier: Bronze 40% customer/ 60%.

insurance company, Silver 30 %customer/ 70% insurance company, Gold 20 %consumer/ 80 %insurance provider, Platinum 10 %customer/ 90 %insurance company, These are high-level numbers across the whole of the plan, taking into consideration the deductible, coinsurance, and copayments, as dictated by the particular structure of the plan, based upon the expected average use of the strategy. These portions do not take premiums into account - What does homeowners insurance cover. In general, Bronze plans have the most affordable regular monthly premiums and Platinum have the highest, with Silver and Gold occupying the price points in between. As you can see from the cost-sharing split above, Bronze plan premiums are cheaper because the consumer pays more expense for healthcare services.

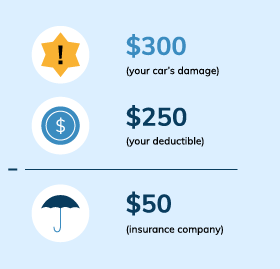

If you frequently use healthcare services, you'll most likely wind up paying more out-of-pocket if you choose a Bronze strategy, even though it has a lower premium. If you qualify, you can utilize a health insurance premium subsidy to help you manage a plan in a higher tier, ultimately saving you money. Catastrophic plans have extremely high deductibles typically, the deductible is the same as the out-of-pocket max which suggests they're actually only helpful for preventing an accident or major disease from causing you to go into serious debt. Catastrophic strategies are just readily available for individuals under 30 or individuals with a hardship exemption. You can not use a subsidy on catastrophic plan premiums, but, for years during which the medical insurance required was active, disastrous plans did count as certifying healthcare. When you purchase a health insurance coverage plan, it is very important to understand what the crucial functions are that decide just how much you're in fact going to pay for healthcare. Each month, you pay a premium to a medical insurance company in order to access a health insurance strategy. As we'll get into in a 2nd, while your regular monthly premium may be how much you spend for medical insurance, it's not equivalent to just how much you pay on healthcare services. In reality, selecting a strategy bluegreen vacation cancellation letter with lower premiums will likely mean that you'll pay more out-of-pocket if you require to see a physician. A deductible is just how much you need to pay for health care services out-of-pocket before your health insurance kicks in. In the majority of strategies, once you pay your deductible, you'll still need to pay copays and coinsurance up until you struck the out-of-pocket max, after which the strategy spends for 100 %of services. Note that the deductible and out-of-pocket optimum explain 2 different concepts: the deductible is just how much you'll spend for a covered procedure before your insurance starts to pay, and the out-of-pocket maximum is the overall quantity you'll spend for care consisting of the deductible. A copayment, typically reduced to simply" copay," is a set quantity that you spend for a particular service or prescription medication. Copayments are one of the methods that health insurers will split costs with you after you hit your deductible. In addition to that, you might have copayments on specific services before you hit your deductible. For example, many medical insurance plans will have copayments for physician's sees and prescription drugs before you strike your deductible.